Quick answer

A demat account is an account used to hold eligible securities in electronic or dematerialised form. Instead of receiving paper share certificates, the investor’s holdings are recorded digitally through a recognised depository system. In India, investors access depository services through a registered Depository Participant, commonly called a DP. A demat account stores securities; a trading account is used to place buy and sell orders. The two accounts often work together but perform different jobs.

Investor note

Key Takeaways

A demat account is an electronic holding account for eligible securities. Investors normally open it through a registered Depository Participant, not directly with the depository. NSDL and CDSL are India’s recognised depositories for mainstream securities-market holdings. A demat account and a trading account are different but usually work together. After a delivery purchase is settled, eligible securities are credited to the demat account. A demat account can support holding, transfer, pledge, nomination and freezing functions. Charges, service standards and operating processes can differ between DPs. Investors should monitor statements, alerts, authorisations and contact details regularly.

What is a demat account?

The word demat is short for dematerialised. A demat account converts the idea of physical security certificates into an electronic holding record.

Before dematerialisation became common, investors often received paper certificates as evidence of ownership. Physical certificates could be delayed, damaged, lost, forged or transferred through time-consuming paperwork. The depository system reduced many of these operational difficulties by maintaining securities electronically.

A demat account is often compared with a bank account:

- A bank account records money.

- A demat account records eligible securities.

This analogy is useful, but the two accounts are not identical. Securities may include shares, bonds, government securities, exchange-traded funds and other eligible instruments supported by the depository and intermediary system.

Investor note

A demat account holds securities, not investment advice

Opening a demat account gives you the infrastructure to hold investments. It does not tell you what to buy, whether a security is suitable or whether the price will rise.

Why is a demat account needed?

A demat account is important because modern securities ownership and transfer are largely electronic.

It can help an investor:

- Hold eligible securities in one electronic account.

- Receive shares purchased for delivery after settlement.

- Deliver shares when selling eligible holdings.

- Receive securities arising from bonus issues, stock splits or other applicable corporate actions.

- Pledge eligible securities subject to the applicable process.

- Transfer securities to another eligible demat account.

- Use nomination and transmission facilities.

- Review balances and transaction statements.

- Freeze the account, selected securities or specified quantities where supported.

For normal delivery-based participation in listed shares, the demat account is a central part of the process.

Who operates the demat system in India?

India’s depository ecosystem includes:

- The investor or beneficial owner

- The Depository Participant

- The depository

- Issuers and registrars

- Stockbrokers, exchanges and clearing corporations

- Banks and other connected intermediaries

The most important beginner distinction is between the depository and the Depository Participant.

Depository

A depository provides the infrastructure for holding and transferring securities electronically. NSDL and CDSL are the two widely recognised depositories in India’s mainstream securities market.

Depository Participant

A Depository Participant is an agent or service interface of a depository. Investors open demat accounts through DPs. Banks, brokers and other eligible institutions may act as DPs when registered and authorised for that role.

Beneficial owner

The person or entity whose securities are recorded in the demat account is commonly called the beneficial owner.

| Participant | Role | Beginner-friendly meaning |

|---|---|---|

| Investor or beneficial owner | Owns the securities recorded in the account | The account holder |

| Depository Participant | Provides demat services to investors | The service point through which the account is opened and operated |

| Depository | Maintains the electronic securities infrastructure | The central record-keeping and transfer system |

| Issuer company | Issues shares or other securities | The company whose security is held |

| Registrar and Transfer Agent | Supports issuer records and corporate-action processing | Connects issuer records with investor entitlements |

| Stockbroker | Provides access to market trading | The intermediary used to place orders |

| Clearing corporation | Calculates and manages settlement obligations | Helps ensure trades move toward completion |

NSDL vs CDSL

NSDL and CDSL are depositories. A beginner does not normally choose a depository in the same way that an investor chooses a share. The DP’s arrangement determines whether the demat account is opened within the NSDL or CDSL system.

| Point | NSDL | CDSL |

|---|---|---|

| Basic role | Electronic holding and transfer of securities | Electronic holding and transfer of securities |

| Investor access | Through registered Depository Participants | Through registered Depository Participants |

| Account identification | Uses depository-specific account structure | Uses depository-specific account structure |

| Core purpose | Safe electronic record keeping and transfer | Safe electronic record keeping and transfer |

| Investment return advantage | None | None |

Demat account vs trading account

The terms are often used together, which causes confusion.

A demat account holds eligible securities. A trading account is used to place orders through a broker.

| Point | Demat account | Trading account |

|---|---|---|

| Main purpose | Holds eligible securities electronically | Places buy and sell orders |

| Connected infrastructure | Depository through a DP | Exchange through a registered broker |

| Used when buying for delivery | Receives the securities after settlement | Sends the purchase order |

| Used when selling delivery holdings | Delivers the securities through the applicable authorisation | Sends the sale order |

| Can hold cash? | It is not a normal bank account | May show trading ledger balances but does not replace a bank account |

| Can hold shares? | Yes, eligible holdings are recorded here | No, the trading account is not the final custody record |

| Simple analogy | Digital locker | Order-control panel |

Worked example

Buying ten shares

Ravi wants to buy ten shares for delivery.

1. Ravi places the order through his trading account. 2. The broker sends the order to the exchange. 3. The trade executes when a suitable seller is available. 4. Clearing and settlement follow. 5. The ten shares are credited to Ravi’s demat account after the applicable settlement process.

The trading account handled the order. The demat account records the resulting holding.

How does a demat account work?

A demat account works through electronic credits and debits.

Credit

When eligible securities enter the account, the holding is credited. This can happen after:

- A delivery purchase

- An IPO allotment

- A bonus issue

- A transfer from another demat account

- A transmission or corporate-action process

- Dematerialisation of eligible physical securities

Debit

When eligible securities leave the account, the holding is debited. This can happen after:

- A delivery sale

- A transfer to another demat account

- A tender under an eligible corporate action

- A rematerialisation request

- A pledge invocation or other authorised process

The investor should receive or review applicable alerts and statements for these movements.

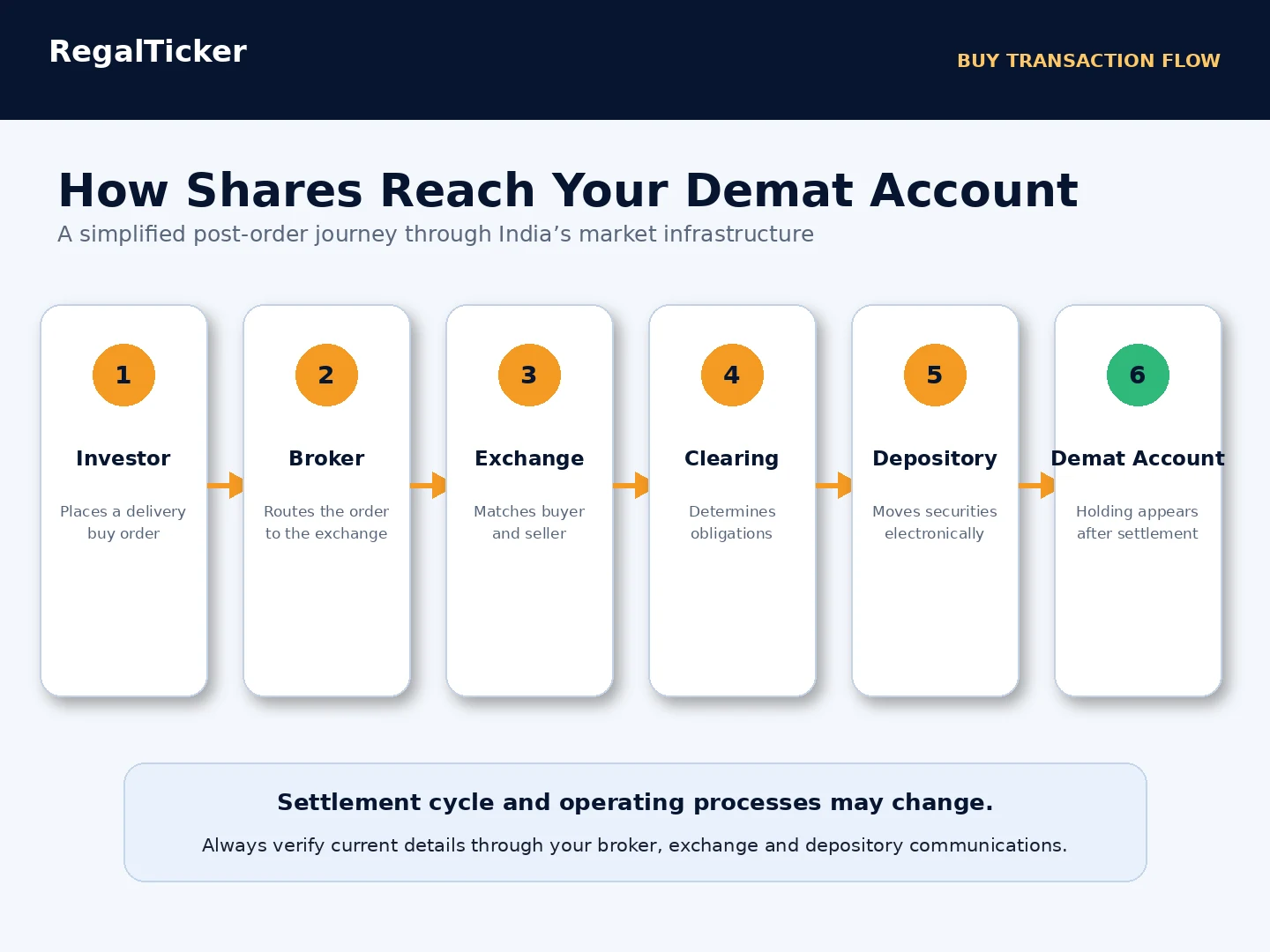

How do purchased shares reach a demat account?

The process involves more than the investor and broker.

Simplified delivery-purchase flow

- The investor places a delivery buy order through the broker.

- The broker routes the order to the selected exchange.

- The exchange matches the order with a compatible sell order.

- The clearing corporation determines the obligations.

- Funds and securities move through the applicable settlement process.

- The depository system credits the purchased securities to the investor’s demat account.

The exact settlement cycle, cut-off times and operating processes may change. Investors should verify current details through official exchange, depository and broker communications.

Risk warning

An executed order is not the same as a settled holding

A trade can be executed before the securities appear in the demat account. Do not assume that a newly purchased delivery holding is available for every purpose until the applicable settlement and credit process is complete.

What can be held in a demat account?

A demat account may support different eligible securities, depending on the depository, DP and instrument.

Examples can include:

- Equity shares

- Preference shares

- Bonds and debentures

- Government securities

- Sovereign gold bonds

- Exchange-traded funds

- Mutual-fund units held in demat form

- Rights entitlements

- Other eligible market instruments

Not every financial product must be held in demat form, and some investments can be maintained through alternative record-keeping systems.

How do you open a demat account?

The exact process varies by DP, but the general steps are similar.

- Select a registered Depository Participant.

- Review charges, services and grievance arrangements.

- Complete account-opening and KYC details.

- Provide the required identity, address, bank and contact information.

- Complete verification through the supported process.

- Review nomination choices and account terms.

- Receive the account identifiers and welcome information.

- Activate login and security controls.

- Verify that the account details are correct.

Commonly requested information may include PAN, identity and address details, bank details, mobile number, email address and income-range information, subject to current requirements.

Investor note

Verify the intermediary

Use official SEBI, exchange, depository or intermediary directories to verify registrations. Do not open accounts through unknown applications, unverified links or people promising guaranteed returns.

What documents are commonly required?

The exact list depends on the investor category and current rules.

| Information or document | Why it may be required |

|---|---|

| PAN | Tax and identity-linked securities-market compliance |

| Identity proof | Verifies the account holder |

| Address proof | Confirms the registered address |

| Bank proof | Links the account for funds and corporate benefits |

| Mobile number | OTP, alerts and communication |

| Email address | Statements, alerts and notices |

| Photograph or digital identity verification | Supports account-opening verification |

| Income information | May be required for specified market segments or risk categories |

| Nomination details or declaration | Records the investor’s nomination choice |

What is a DP ID, Client ID and BO ID?

A demat account is identified through depository-specific numbers.

- DP ID: Identifies the Depository Participant.

- Client ID: Identifies the investor account within the DP arrangement.

- BO ID: Refers to the beneficial-owner account identifier.

The presentation differs between NSDL and CDSL systems. Investors should copy account numbers carefully when transferring securities or completing forms.

Risk warning

Never guess a demat account number

A wrong account identifier can cause rejection, delay or transfer risk. Verify the DP ID, Client ID, BO ID and ISIN from official statements or the intermediary’s verified interface.

What is an ISIN?

ISIN stands for International Securities Identification Number. It uniquely identifies a specific security.

A company can have more than one security, such as:

- Equity shares

- Preference shares

- Debentures

- Partly paid shares

- Different classes of instruments

The company name alone may not be enough. The ISIN helps identify the exact security being credited, debited, transferred or pledged.

What are dematerialisation and rematerialisation?

Dematerialisation

Dematerialisation is the process of converting eligible physical security certificates into electronic form.

The investor generally submits the certificates and request through the DP. The issuer or registrar verifies the request, and eligible securities are credited electronically after completion.

Rematerialisation

Rematerialisation is the reverse process—converting eligible demat holdings into physical certificates, subject to the applicable process and availability.

For most modern retail investors, electronic holdings are more practical, but the exact facility depends on the security and current rules.

What are demat account charges?

Charges vary between DPs and service plans.

Potential charges can include:

- Account-opening charge

- Annual maintenance charge

- Debit transaction charge

- Dematerialisation or rematerialisation charge

- Pledge-related charge

- Statement or special service charge

- Off-market transfer charge

Some services may be free or bundled, while others may carry conditions.

| Charge question | What to check |

|---|---|

| Account opening | Is there a one-time charge? |

| Annual maintenance | Is it fixed, tiered or waived under conditions? |

| Debit transaction | Is there a charge when securities leave the account? |

| Pledge services | What are creation, closure and invocation charges? |

| Statements | Are electronic statements free? |

| Closure and transfer | Are there charges for moving holdings or closing the account? |

| Taxes | Are applicable taxes added to the quoted fee? |

What is a Basic Services Demat Account?

A Basic Services Demat Account, commonly called a BSDA, is a simplified demat facility intended for eligible individual investors under specified conditions.

It may offer reduced maintenance charges based on current eligibility and holding-value rules. Because thresholds and conditions can change, investors should verify the latest SEBI and DP information rather than relying on old figures.

Can you have more than one demat account?

An investor may be able to maintain multiple demat accounts, subject to KYC, intermediary and regulatory requirements.

Possible reasons include:

- Separating long-term and active holdings

- Using different brokers or service providers

- Maintaining individual and joint accounts

- Managing different investment strategies

Multiple accounts can also increase record-keeping work, charges and nomination responsibilities.

Investor note

More accounts do not create more ownership

If you own 100 shares across two demat accounts, you still own 100 shares in total. Additional accounts change the record structure, not the economic quantity.

Can a demat account be opened jointly?

Joint demat accounts may be available, subject to the DP’s process and account-opening rules.

The order and names of joint holders matter. The ownership pattern must be handled carefully for transfers, dematerialisation, nomination and transmission.

A joint demat account is not the same as adding a nominee.

What is nomination in a demat account?

Nomination allows the account holder to identify one or more persons for the applicable transmission process after the holder’s death, subject to current rules and legal requirements.

Nomination does not automatically resolve every inheritance issue, but keeping nomination details updated can reduce operational difficulty.

Investors should:

- Make a valid nomination choice.

- Review the names and percentages where applicable.

- Update details after major life events.

- Keep nominees informed about the account.

- Preserve account and intermediary information securely.

What is a Consolidated Account Statement?

A Consolidated Account Statement can provide a combined view of eligible securities and investments associated with the investor’s identifiers across participating systems.

It can help an investor:

- Review holdings

- Detect unknown transactions

- Compare records

- Track corporate-action credits

- Identify inactive accounts

- Support family financial records

The investor should read statements rather than assuming that mobile-app figures are always complete.

What is DDPI?

DDPI refers to Demat Debit and Pledge Instruction. It is an authorisation framework that can allow a broker or intermediary to debit or pledge securities for specified purposes, subject to its terms and applicable rules.

An investor should understand:

- What actions are authorised

- Whether the authorisation is optional

- How it can be revoked or modified

- Whether a transaction can instead be authorised through electronic instructions

- Which securities and purposes are covered

Risk warning

Do not sign broad authorisations without reading them

A convenient instruction can affect control over securities. Review the scope, purpose and revocation process before authorising any debit, pledge or transfer arrangement.

What is a pledge in a demat account?

A pledge creates a security interest over eligible holdings, often for collateral or borrowing-related purposes.

Pledged securities remain subject to the pledge arrangement until release, closure or invocation under the applicable conditions.

The investor should understand:

- The purpose of the pledge

- The quantity and ISIN

- The lender or pledgee

- Haircuts and collateral value

- Margin calls

- Invocation risk

- Charges and release procedure

Pledging does not remove market risk. If the security price falls, additional collateral may be required.

Can a demat account be frozen?

Depository systems may support freezing the entire account, specific securities or specified quantities, depending on the available facility.

A freeze can help prevent unauthorised debits while allowing the account to remain recorded.

Investors may consider asking the DP about freeze options when:

- The account will not be used for a long period.

- A security concern is suspected.

- A legal or operational restriction is needed.

- The investor wants to limit debits temporarily.

Freezing does not protect against changes in market value.

Demat account safety checklist

Essential security habits

- Never share OTPs, passwords, PINs or authentication codes.

- Use only official apps and verified web addresses.

- Review exchange and depository alerts.

- Reconcile holdings with statements.

- Check unknown credits, debits or pledges immediately.

- Keep mobile, email, bank and address details updated.

- Understand all debit and pledge authorisations.

- Use nomination facilities appropriately.

- Ask about freezing options.

- Report suspected misuse without delay.

Worked example

Why alerts matter

Suppose an investor receives a depository alert for a debit of 500 shares but has not sold or transferred those shares.

The investor should not ignore the message. The correct response is to verify the account immediately, contact the DP and broker through official channels, secure login credentials and use the applicable grievance or reporting process.

What happens if a broker closes?

A demat account’s securities record is maintained through the depository and DP structure. The broker and DP may be the same organisation or related services, but their roles are distinct.

If an intermediary stops operating, investors should follow official depository, exchange and regulatory guidance for transferring holdings or migrating services.

The investor should keep:

- Client master details

- Latest holding statement

- Transaction statements

- Contract notes

- Bank records

- Nomination details

- Official intermediary communication

Can money be kept in a demat account?

A demat account is not a normal cash account. It records eligible securities.

Money used for investments is handled through bank and trading-ledger arrangements. Corporate cash benefits, such as eligible dividends, are generally credited through the registered bank arrangement, subject to the issuer and payment process.

Common myths about demat accounts

Myth 1: A demat account is the same as a trading account

It is not. The demat account holds eligible securities; the trading account places market orders.

Myth 2: The broker owns the shares in my demat account

The investor is recorded as the beneficial owner, subject to the applicable account structure and valid encumbrances.

Myth 3: A demat account guarantees safe investments

It improves electronic custody and record keeping. It does not prevent a poor security from losing value.

Myth 4: Zero account-opening fee means zero total cost

Other charges may still apply, including maintenance, debit, pledge or service charges.

Myth 5: A dormant account requires no monitoring

Inactive accounts can still contain valuable holdings and personal information. Statements, contact details and security should be reviewed.

Myth 6: Every investment must be held in demat form

Some products can exist in demat form, statement-of-account form or other record systems. The available holding method depends on the product.

Beginner checklist before opening a demat account

- Verify the DP and related broker registrations.

- Compare the complete charge schedule.

- Review app security and service channels.

- Understand whether the account is with NSDL or CDSL.

- Complete KYC carefully.

- Add and verify bank details.

- Make an informed nomination choice.

- Read debit, pledge and DDPI authorisations.

- Save account identifiers and welcome documents.

- Test login, alerts and statement access.

- Understand the grievance process.

- Review the account after the first transaction.

Frequently asked questions

What is a demat account in simple words?

A demat account is an electronic account used to hold eligible securities such as shares in digital form instead of paper certificates.

Is a demat account the same as a trading account?

No. A trading account places buy and sell orders, while a demat account records electronic holdings.

Who opens a demat account?

Investors open demat accounts through registered Depository Participants connected to a recognised depository.

What are NSDL and CDSL?

They are depositories that provide electronic securities holding and transfer infrastructure through their Depository Participants.

Can I buy shares without a demat account?

For normal delivery-based electronic holding of listed shares, a demat account is generally required. Other products and transaction types can follow different arrangements.

Can I have multiple demat accounts?

Multiple accounts may be allowed, subject to current rules and intermediary requirements. Each account should be monitored and may have separate charges.

Does a demat account hold cash?

No. It records securities. Cash moves through bank and trading-ledger arrangements.

Are shares safe if they are in demat form?

Demat form reduces many physical-certificate risks, but investors must still protect credentials, monitor alerts and understand pledges or authorisations.

What happens after I buy a share?

After execution and the applicable settlement process, eligible delivery securities are credited to the demat account.

What should I learn next?

The next useful guide is What Is a Trading Account and How Does It Work?

Conclusion

A demat account is the electronic ownership record behind modern securities investing in India. It works through depositories such as NSDL and CDSL, while Depository Participants provide account services to investors.

The demat account does not choose investments or guarantee returns. Its job is to record, transfer and support the electronic handling of eligible securities.

A beginner should understand four separate roles:

- The bank account handles money.

- The trading account places orders.

- The stock exchange matches eligible orders.

- The demat account records the resulting securities holdings.

Good investing therefore requires both sound investment judgment and careful account management.

Continue learning in Demat & Trading

After understanding where securities are held, continue with these connected guides:

These articles explain how orders are placed, how money moves and why the three-account structure matters.

Verify through official sources

Official references

- SEBI Investor — Securities Market Investment: Start Investing

- SEBI Investor — Difference Between Depository and Depository Participant

- SEBI Investor — Investor Education Material

- SEBI Investor — Do’s and Don’ts of Investing

- SEBI Investor — Market Infrastructure Institutions

- NSDL — e-Guide for Demat Account Holders

- NSDL — Investor Charter

- CDSL — Open a Demat Account

- CDSL — Investor Charter

- NSE — Opening an Account

Educational disclaimer: This article is for investor education and general information only. It does not constitute investment advice, a research recommendation, an invitation to trade, an offer to buy or sell securities, or an assurance of returns. Account-opening requirements, KYC rules, settlement cycles, charges and intermediary processes can change. Readers should verify current information through SEBI, depositories, exchanges and their registered intermediary before acting.